US Census Bureau –

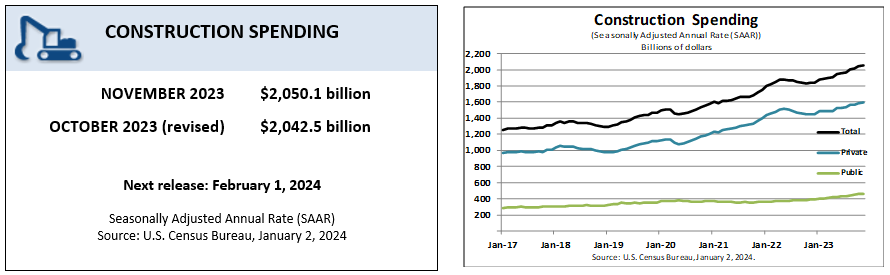

Total Construction

Construction spending during November 2023 was estimated at a seasonally adjusted annual rate of $2,050.1 billion, 0.4 percent (±1.0 percent)* above the revised October estimate of $2,042.5 billion. The November figure is 11.3 percent (±1.5 percent) above the November 2022 estimate of $1,842.2 billion. During the first eleven months of this year, construction spending amounted to $1,817.1 billion, 6.2 percent (±1.0 percent) above the $1,711.1 billion for the same period in 2022.

Private Construction

Spending on private construction was at a seasonally adjusted annual rate of $1,595.0 billion, 0.7 percent (±0.5 percent) above the revised October estimate of $1,584.4 billion. Residential construction was at a seasonally adjusted annual rate of $896.8 billion in November, 1.1 percent (±1.3 percent)* above the revised October estimate of $887.3 billion. Nonresidential construction was at a seasonally adjusted annual rate of $698.2 billion in November, 0.2 percent (±0.5 percent)* above the revised October estimate of $697.1 billion.

Public Construction

In November, the estimated seasonally adjusted annual rate of public construction spending was $455.1 billion, 0.7 percent (±1.8 percent)* below the revised October estimate of $458.1 billion. Educational construction was at a seasonally adjusted annual rate of $99.2 billion, 0.3 percent (±2.0 percent)* below the revised October estimate of $99.5 billion. Highway construction was at a seasonally adjusted annual rate of $135.8 billion, 0.1 percent (±4.4 percent)* above the revised October estimate of $135.6 billion.

More information on construction spending

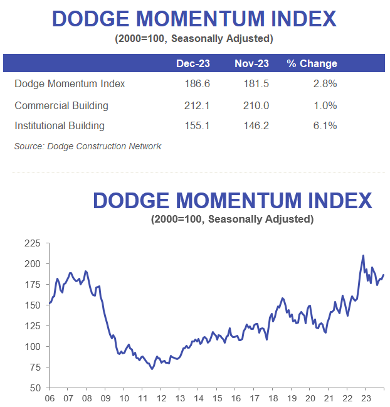

The Dodge Momentum Index (DMI), issued by Dodge Construction Network, rose 3% in December to 186.6 (2000=100) from the revised November reading of 181.5.

Over the month, commercial planning grew 1.0% and institutional planning improved 6.1%.

“The Momentum Index ended the year 11% below the November 2022 peak, ultimately stabilizing as the year progressed. Regardless, the DMI averaged a reading of 184.3 in 2023, hitting levels of activity that haven’t been recorded since 2008,” stated Sarah Martin, associate director of forecasting for Dodge Construction Network. “While ongoing labor and construction cost issues will persist in 2024, a substantive amount of projects are sitting in the planning queue and will support construction spending going into 2025.”

Hotel and data center planning drove growth in the commercial segment of the DMI over the month of December, while stronger healthcare and public building planning supported more momentum on the institutional side. Year over year, the DMI was 2% lower than in December 2022. The commercial segment was down 9% from year-ago levels, while the institutional segment was up 14% over the same time period.

A total of 23 projects valued at $100 million or more entered planning in December, with six valued over $400 million. The largest commercial projects include the $500 million Universal Theme Park Kids Resort and Hotel in Frisco, Texas, and the $400 million Dog River Industrial Park in Mobile, Alabama. The largest institutional projects include two Mayo Clinic buildings, each valued at $400 million, in Rochester, Minnesota.

The DMI is a monthly measure of the value of nonresidential building projects going into planning, shown to lead construction spending for nonresidential buildings by a full year.

Watch Associate Director of Forecasting Sarah Martin discuss December’s DMI here.

ABC

Construction input prices decreased 0.6% in December compared to the previous month, according to an Associated Builders and Contractors analysis of U.S. Bureau of Labor Statistics’ Producer Price Index data released today. Nonresidential construction input prices decreased 0.4% for the month.

Overall construction input prices are 1.2% higher than a year ago, while nonresidential construction input prices are 1.6% higher. Prices decreased in 2 of the 3 energy subcategories last month. Crude petroleum input prices were down 13.2%, while unprocessed energy materials were down 9.1%. Natural gas prices rose 1.5% in December.

“Construction input prices fell sharply in December,” said ABC Chief Economist Anirban Basu. “While plunging oil prices are the primary factor behind the sharp decline, most input prices were tame in 2023’s final month. That serves as a fitting end to a year during which aggregate input prices increased just 1.2% and many individual commodity prices actually fell.

“Despite continued materials price moderation and other positive developments regarding inflation, the outlook is not without risks,” said Basu. “Piracy in the Red Sea and the resulting diversion of ships from the Suez Canal around the Cape of Good Hope has caused global freight rates to nearly double in the first two weeks of 2024, according to the Freightos Baltic Index. All else equal, rising shipping costs will put upward pressure on certain inputs.”

Construction Industry Adds 17,000 Workers In December But Association Survey Finds Contractors Are Struggling To Find Skilled Employees

Hourly Wages for Production Workers Climb 5.1 Percent over the Year, Outpacing Overall Private Sector; Association Survey Finds Most Contractors Plan to Add to Headcount in 2024 but Anticipate Difficulty

The construction sector added 17,000 employees in December and continued to raise wages at a faster clip than other industries, the Associated General Contractors of America reported in an analysis of government data released today. Association officials said the survey it released this week found contractors expect to hire more employees in 2024 but are struggling to find enough qualified workers.

“The above-average wages that the construction industry pays have helped contractors add workers,” said Ken Simonson, the association’s chief economist. “More than two-thirds of firms in our survey say they plan to expand in 2024 but they expect it will be as hard or harder to do than it was in 2023.”

Construction employment in December totaled 8,056,000, seasonally adjusted, an increase of 17,000 from November. The sector has added 197,000 jobs during the past 12 months. That was a gain of 2.5 percent, which outpaced the 1.7 percent job growth in the overall economy. Residential building and specialty trade contractors added 5,500 employees in December and 40,100 (1.2 percent) over 12 months. Employment at nonresidential construction firms—nonresidential building and specialty trade contractors along with heavy and civil engineering construction firms—climbed by 11,900 positions for the month and 157,300 (3.4 percent) since December 2022.

Average hourly earnings for production and non-supervisory employees in construction—covering most onsite craft workers as well as many office workers—climbed by 5.1 percent over the year to $34.92 per hour. Construction firms in December provided a wage “premium” of nearly 19 percent compared to the average hourly earnings for all private-sector production employees.

In a survey the association released on Thursday, 69 percent of the nearly 1300 responding construction firms reported they expect to add to their headcount in 2024, while only 10 percent expect to reduce headcount. But 55 percent of respondents, including both union and open-shop employers, expect it will be as hard or harder to do so than in 2023.

Association officials observed that contractors will have trouble completing the infrastructure, renewable energy, and advanced manufacturing projects the Biden administration is counting on unless they can hire enough skilled workers. They urged officials in Washington to reform employment-based immigration policies and boost funding for career and technical education programs that will enable more people to qualify for rewarding jobs in construction.

“Contractors are eager to build the structures that will sustainably improve the nation’s productivity and quality of life,” said Stephen E. Sandherr, the association’s chief executive officer. “Limiting who can work in construction undercuts the sector’s ability to deliver projects on time and on budget.”

Read A Construction Market in Transition: The 2024 Construction Hiring & Business Outlook. Check out the survey results. Watch a quick video about the results. Here’s an employment table.