The Dodge Momentum Index (DMI),

issued by Dodge Construction Network, declined 2.5% in June to 197.3 (2000=100) from the revised May reading of 202.4. Over the month, the commercial component of the DMI rose 3.1%, while the institutional component sank 10.5%.

“A deceleration in institutional planning caused the Momentum Index to decrease in June,” said Sarah Martin, associate director of forecasting for Dodge Construction Network. “Project activity in this segment pulled back from the robust highs of the last three months but continued to dwarf year-ago levels. In contrast, growth in the commercial segment may be fleeting, as the continued elevation in interest rates and increasingly tight lending standards weigh down the sector in the latter half of the year.”

U.S. Census Bureau

Total Construction

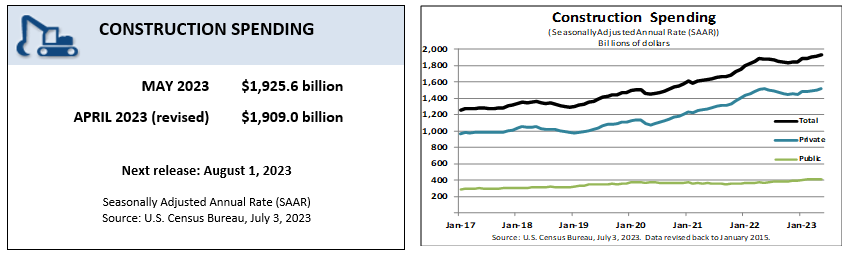

Construction spending during May 2023 was estimated at a seasonally adjusted annual rate of $1,925.6 billion, 0.9 percent (±0.5 percent) above the revised April estimate of $1,909.0 billion. The May figure is 2.4 percent (±1.2 percent) above the May 2022 estimate of $1,880.9 billion. During the first five months of this year, construction spending amounted to $740.8 billion, 2.9 percent (±1.0 percent) above the $719.6 billion for the same period in 2022.

ABI May 2023: Architecture firm billings bounce back

Nearly half of firm leaders think architecture staff productivity has declined compared to pre-pandemic levels

Business conditions at architecture firms bounced back in May, following a modest downturn in April. The AIA/Deltek Architecture Billings Index (ABI) score for the month was 51.0, the highest it has been since last September. In addition, inquiries into new projects and the value of new design contracts also bounced back this month, with inquiries reaching their highest level in nine months, and design contracts increasing for the first time since February. With recent declines in inflation and a pause in interest rate increases, it appears that the economy may be stabilizing.

Despite growth in the overall ABI this month, business conditions remain variable in different regions of the country. Billings improved at firms located in the South for the second consecutive month in May, while they were essentially flat at firms located in the Midwest, following six months of growth. However, billings continued to decline at firms located in both the West and Northeast, where scores have been below 50 since last fall. By firm specialization, business conditions softened further at firms with a multifamily residential specialization in May, falling to the lowest level in two years. Billings also declined for the ninth consecutive month at firms with a commercial/industrial specialization. On the other hand, business conditions improved for the second month in a row at firms with an institutional specialization, as they reported their strongest growth since last year.

ENR – Construction Cost Index:

AGC:

Construction Firms Add 23,000 Jobs In June As Sector’s Unemployment Rate Sets 24-year Low Of 3.6 Percent And Craft Workers’ Hourly Pay Tops $34

The construction sector added 23,000 jobs in June while the sector’s unemployment rate fell to the lowest rate ever for the month and pay levels in the industry continued to rise, according to an analysis of new government data the Associated General Contractors of America released today. Association officials said there appears to be plenty of demand for construction services and that employers likely would have added even more jobs if they could find more workers to hire.

“There was no letup in demand for construction workers in June, while the supply of available workers remained exceptionally tight,” said Ken Simonson, the association’s chief economist. “Both residential and nonresidential construction are expanding despite concerns about overall economic growth and inflation.” Read more.

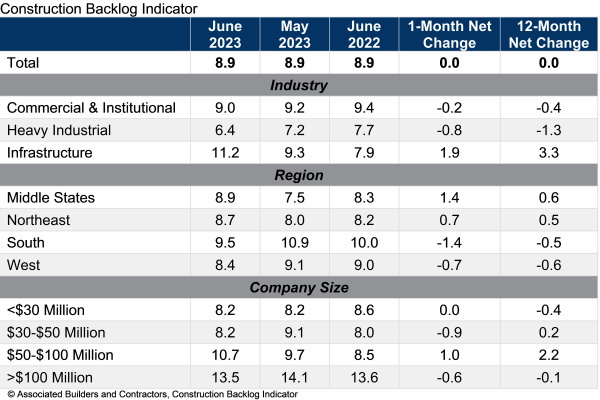

ABC’s Construction Backlog Indicator Steady in June, Contractor Confidence Down

Associated Builders and Contractors reported on July 11 that its Construction Backlog Indicator remained unchanged at 8.9 months in June, according to an ABC member survey conducted June 20 to July 5. The reading is unchanged from June 2022.

View the historic Construction Backlog Indicator and Construction Confidence Index data series.

Backlog in the infrastructure category increased for the third straight month and is now at the highest level in nearly two years. On a regional basis, the South remains the region with the highest backlog, despite being the only region in which backlog declined in June.

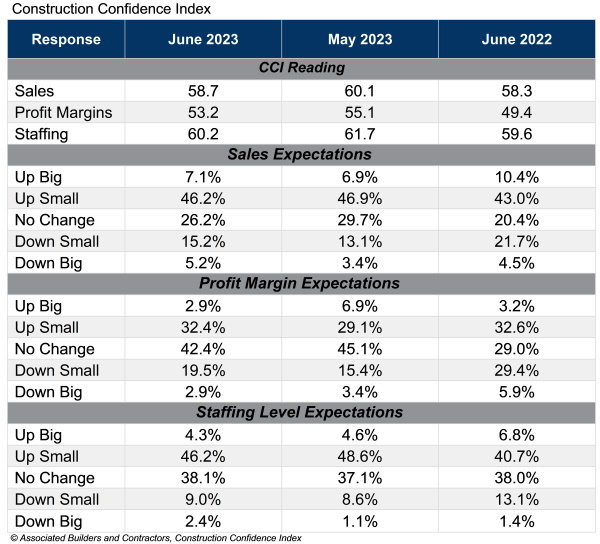

ABC’s Construction Confidence Index reading for sales, profit margins and staffing levels moved lower in June. All three readings remain above the threshold of 50, indicating expectations of growth over the next six months.

Note: The reference months for the Construction Backlog Indicator and Construction Confidence Index data series were revised on May 12, 2020, to better reflect the survey period. CBI quantifies the previous month’s work under contract based on the latest financials available, while CCI measures contractors’ outlook for the next six months.