The latest reading from the National Federation of Independent Business’s Small Business Optimism Index notched up from 91.0 in June to 91.9 in July–the highest level of 2023 so far. Still, that remains historically low, with July marking the 19th consecutive month below the 49-year average of 98.

The latest gross domestic product report from the Bureau of Economic Analysis showed that consumer spending still drove much of the increase in U.S. economic growth in the second quarter, even though spending did decelerate from the first quarter overall.

That strength is due at least in part to a resilient labor market and low unemployment that’s given workers some cash to spend. The July jobs report shows that employers added the fewest number of jobs so far this year at 187,000, but economists say that’s still a solid report.

Continued demand for talent helps explain why a net 38 percent of business owners raised wages in July – up two points from June.

DODGE MOMENTUM INDEX

The Dodge Momentum Index (DMI), issued by Dodge Construction Network, declined 0.9% in July to 193.4 from the revised June reading of 195.1. Over the month, the commercial component of the DMI remained relatively flat, ticking down 0.2%, while the institutional component fell 1.9%.

The DMI is a monthly measure of the initial report for nonresidential building projects in planning, shown to lead construction spending for nonresidential buildings by a full year.

All commercial sectors pulled back, or remained flat, over the month of July. Hotel planning saw the largest month-over-month decay, marking four months of consecutive decline in the sector. July also saw a deceleration in the number of education and healthcare projects entering planning, the two largest institutional segments. While two sizable public projects entered planning and pushed activity in the sector to double-digit gains, it was not enough to push the institutional portion of the index positive. Year over year, the DMI remains 21% higher than in July 2022. The commercial and institutional components were up 13% and 35%, respectively.

PPI Shows Many Construction Material Prices Are Stabilizing, Analysts Say

Prices for many construction materials have stabilized and some have begun dropping, although costs still remain higher than since the start of the COVID-19 pandemic, according to industry group analyses of the latest U.S. Bureau of Labor Statistics Producer Price Index data released Aug. 11.

Inputs to nonresidential construction fell by 0.1% in July and were down 2.7% over the past 12 months, according to the Associated Builders and Contractors. But those inputs were still up 39.1% compared to February 2020, before the coronavirus severely impacted supply chains. Anirban Basu, ABC chief economist, attributed the price stagnation to improved supply chains and a “sluggish global economy.” He predicted that most construction material prices, not including energy prices, should be mostly stable in the coming months. More…

2023 National Construction Survey by Marcum

The construction industry is grappling with the implications of rising interest rates, inflation and changing economic dynamics, according to the 2023 National Construction Survey by Marcum Construction Services. The annual survey covers a range of topics, from top priorities to problems, strategies, possible solutions and the influence of a potential recession on the industry. The 2023 edition is the fourth iteration of Marcum’s national industry study.

Key findings

Among this year’s key findings, companies are struggling with rising inflation and interest rates, with 50% expecting project delays or cancellations. Over half anticipate difficulty in passing expenses onto customers.

- Increasing Costs: 60% of respondents report higher general and administrative overhead expenses than in the past year.

- Taxes: Despite being the third-most important political issue, only 26% of companies are leveraging the Research and Development tax credit, suggesting potential lost opportunities.

- Skilled Labor Shortage: 39% cite securing skilled labor as their biggest threat in the coming year, up from 27% in 2022. Labor costs are also seen as a significant threat, doubling to 14% from the previous year.

- Pessimistic Outlook: Just 37% of respondents expect more project opportunities in their regions in the coming year, down from 59% last year. Those expecting fewer opportunities doubled to 26% this year.

- Recession Preparedness: 80% are focused on managing cash flow, and 59% are planning around a potential recession, up from 49% last year.

- Priorities Shift: There’s a marked increase in companies focusing on cost-cutting and sourcing skilled labor, with both seeing all-time highs of 47% and 50%, respectively.

- Healthy Backlogs Despite Challenges: Despite challenges, backlogs remain healthy. Companies are being more selective when bidding on projects due to a reduction in the number of competing bidders.

More than most, construction firms feel the sting of higher lending rates. Respondents in the survey pointed to a significant decline in the ease of obtaining financing, down to 4% from 19% last year. The survey also indicates increased difficulty in obtaining bonding. This issue is especially acute for firms with leveraged balance sheets and thin capital.

Despite the challenges, the industry outlook is far from bleak. The survey reveals that the construction industry is showing impressive resilience. Just 32% of respondents are expecting a lower backlog this year, and those expecting a higher backlog are at 41% this year, just a 7% drop from the previous year.

Additionally, supply chains have improved, and material costs are stabilizing, with some sectors reporting declines. A sustained demand for skilled labor indicates underlying economic robustness.

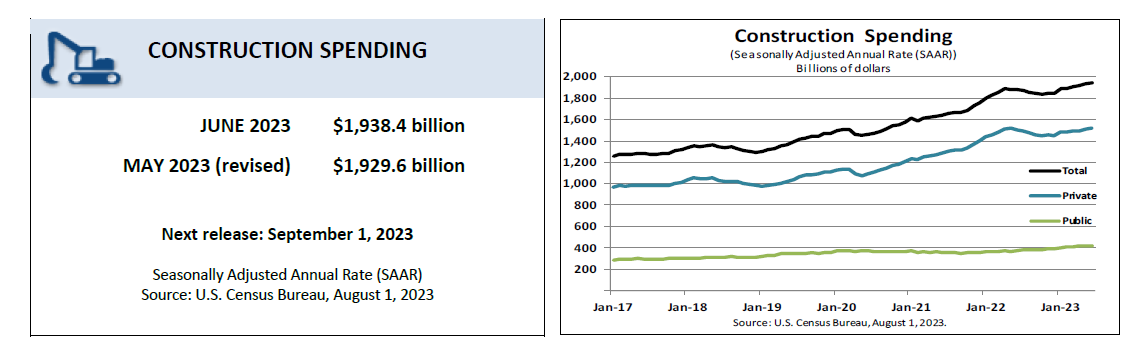

Construction

Construction spending during June 2023 was estimated at a seasonally adjusted annual rate of $1,938.4 billion, 0.5 percent (±0.5 percent)* above the revised May estimate of $1,929.6 billion. The June figure is 3.5 percent (±1.3 percent) above the June 2022 estimate of $1,873.2 billion. During the first six months of this year, construction spending amounted to $917.4 billion, 3.0 percent (±1.0 percent) above the $890.4 billion for the same period in 2022.

Private Construction

Spending on private construction was at a seasonally adjusted annual rate of $1,516.9 billion, 0.5 percent (±0.3 percent) above the revised May estimate of $1,509.4 billion. Residential construction was at a seasonally adjusted annual rate of $856.3 billion in June, 0.9 percent (±1.3 percent)* above the revised May estimate of $848.6 billion. Nonresidential construction was at a seasonally adjusted annual rate of $660.6 billion in June, virtually unchanged from (±0.3 percent)* the revised May estimate of $660.8 billion.

Public Construction

In June, the estimated seasonally adjusted annual rate of public construction spending was $421.4 billion, 0.3 percent (±1.0 percent)* above the revised May estimate of $420.2 billion. Educational construction was at a seasonally adjusted annual rate of $88.9 billion, 0.1 percent (±1.5 percent)* below the revised May estimate of $89.0 billion. Highway construction was at a seasonally adjusted annual rate of $128.6 billion, 0.1 percent (±2.6 percent)* below the revised May estimate of $128.6 billion.