U.S. Census

Total Construction

Construction spending during August 2024 was estimated at a seasonally adjusted annual rate of $2,131.9 billion, 0.1 percent (±1.2 percent)* below the revised July estimate of $2,133.9 billion. The August figure is 4.1 percent (±1.6 percent) above the August 2023 estimate of $2,047.4 billion. During the first eight months of this year, construction spending amounted to $1,428.5 billion, 7.6 percent (±1.2 percent) above the $1,327.0 billion for the same period in 2023.

Private Construction

Spending on private construction was at a seasonally adjusted annual rate of $1,642.2 billion, 0.2 percent (±0.7 percent)* below the revised July estimate of $1,645.8 billion. Residential construction was at a seasonally adjusted annual rate of $899.9 billion in August, 0.3 percent (±1.3 percent)* below the revised July estimate of $903.0 billion. Nonresidential construction was at a seasonally adjusted annual rate of $742.2 billion in August, 0.1 percent (±0.7 percent)* below the revised July estimate of $742.8 billion.

Public Construction

In August, the estimated seasonally adjusted annual rate of public construction spending was $489.8 billion, 0.3 percent (±2.0 percent)* above the revised July estimate of $488.2 billion. Educational construction was at a seasonally adjusted annual rate of $102.4 billion, virtually unchanged from (±2.6 percent)* the revised July estimate of $102.3 billion. Highway construction was at a seasonally adjusted annual rate of $141.4 billion, 1.1 percent (±5.4 percent)* above the revised July estimate of $140.0 billion.

ABC

ABC:September sees added jobs

The construction industry added 25,000 jobs on net in September, according to an Associated Builders and Contractors analysis of data released today by the U.S. Bureau of Labor Statistics. On a year-over-year basis, industry employment is up by 238,000 jobs, an increase of 3.0%.

Nonresidential construction employment increased by 17,900 positions on net, with growth in 2 of the 3 subcategories. Nonresidential specialty trade added the most jobs, increasing by 17,000 positions. Heavy and civil engineering added 3,800 jobs while nonresidential building lost 2,900 positions.

The construction unemployment rate increased to 3.7% in September. Unemployment across all industries decreased from 4.2% in August to 4.1% last month.

“The construction industry added jobs for the fifth consecutive month despite labor shortages,” said ABC Chief Economist Anirban Basu. “The industry unemployment rate rose to 3.7% in September, but that’s still lower than in any month on record before the second half of 2018 and half a percentage point below the economywide unemployment rate. Hiring should persist in the coming months, with contractors expecting to increase their staffing levels over the next six months, according to ABC’s Construction Confidence Index.

“Beyond the construction industry, this jobs report blew past expectations,” said Basu. “U.S. employers added 254,000 jobs for the month, the most since March, and employment estimates for the previous two months were revised upward by a total of 72,000 jobs. While the ongoing strength of the labor market and consumer spending indicates that the economy has weathered high interest rates better than anyone thought possible, the combination of rising household debt levels and economic uncertainty surrounding geopolitics and the looming election will potentially weigh on growth.

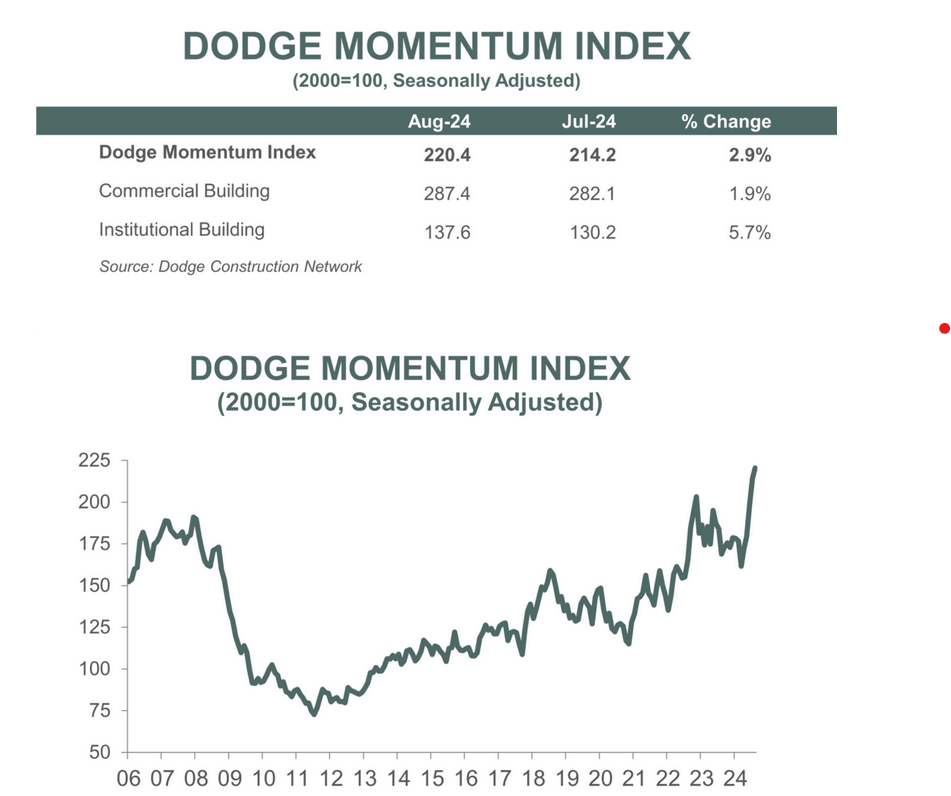

Dodge:

The Dodge Momentum Index (DMI), issued by Dodge Construction Network, increased 2.9% in August to 220.4 (2000=100) from the revised July reading of 214.2. Over the month, commercial planning expanded 1.9% and institutional planning improved 5.7%.

“Owners and developers continued to prime the planning queue in August, ahead of next year’s anticipated stronger market conditions,” stated Sarah Martin, associate director of forecasting at Dodge Construction Network. “With the Fed’s September rate cut all but finalized, the influence of selective lending standards and inflation should moderate next year, alongside a modest upgrade to consumer demand. As a result, stronger planning activity was widespread in August, with most nonresidential sectors seeing growth.”

Commercial planning saw another month of broad-based improvements. After slowing down in recent years, warehouse projects have gained momentum over the last three months. Hotels and retail planning have been steadily expanding as well. Data centers continued to dominate large project activity, but the rate at which planning projects entered the queue in August moderated after several months of very strong growth. On the institutional side, healthcare was the primary driver of this past month’s expansion, followed by recreational planning. In August, the DMI was 31% higher than in August of 2023. The commercial segment was up 42% from year-ago levels, while the institutional segment was up 8% over the same period.

A total of 30 projects valued at $100 million or more entered planning throughout August. The largest commercial projects included the $500 million portion of the Tract Data Center Complex in Yuma, Arizona, and the $462 million KDC Data Center Campus in Irving, Texas. The largest institutional projects to enter planning were the $440 million Geisinger Medical Center Tower in Danville, Pennsylvania and the $240 million academic and research facility at the University of Cincinnati in Ohio.

The DMI is a monthly measure of the value of nonresidential building projects going into planning, shown to lead construction spending for nonresidential buildings by a full year.