Highlights from the latest construction forecasts show that U.S. economic recovery slowly continues, shadowed by inflation and labor challenges, and geopolitical risk

By: Tara Lukasik, Glass Magazine

Editor’s Note: The following is based on forecast presentations from the 2024 Annual Outlook Forecast Conference from Dodge Construction Network, and The Construction Economy Outlook semiannual webcast by ConstructConnect.

Economic uncertainty hung over 2023 and is carrying over to 2024, but many industry experts remain cautiously optimistic about the year ahead, predicting a stronger and more consistent construction market.

1 | Economy on edge but recession-free

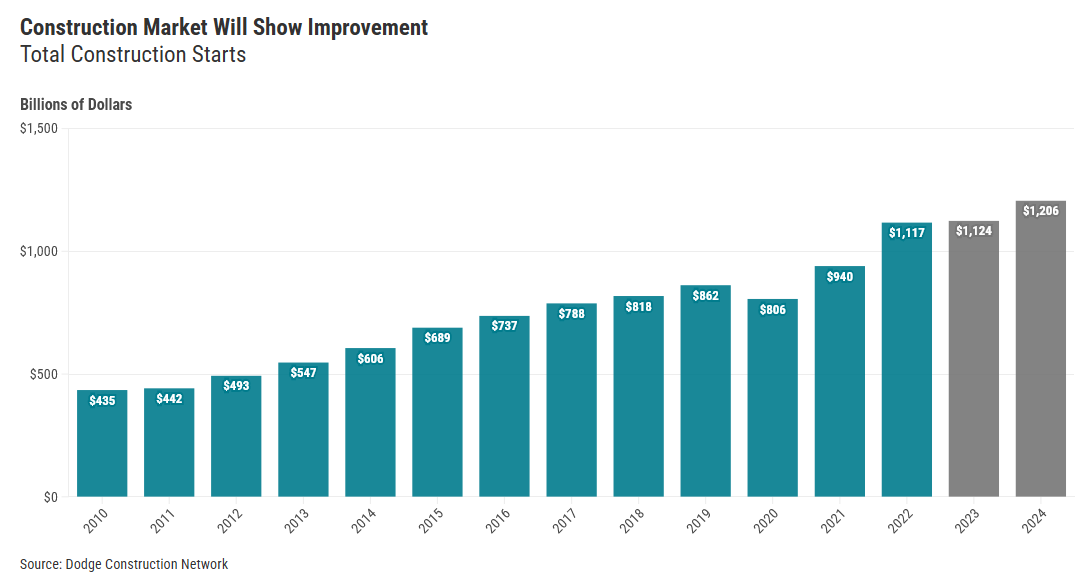

Overall construction starts are expected to rise 7% in 2024, following a 1% increase in 2023, according to the Dodge forecast. The 2023 increase will bring total starts to an estimated $1.124 trillion, with $1.206 trillion forecast for 2024.

In looking at the macroeconomic pressures facing the U.S economy, including stubborn inflation, high interest rates, tight lending standards, labor shortage, rising energy prices and geopolitical turmoil, it’s impressive that the economy has remained recession-free. Resilient consumers, a healthy labor market, and public funding for manufacturing and infrastructure helped, but the challenges of 2023 will shift over into 2024, according to Richard Branch, chief economist for Dodge Construction Network.

“We’re anticipating that 2024 will bring about more consistent growth as well as more opportunity in the construction sector,” says Branch, “but the economy will remain challenged at least over the next three to six months. Still, we’re remaining confident that the U.S. economy will remain recession free.”

However, Branch adds that this is dependent on the assumption that the Federal Reserve is done raising interest rates. Dodge forecasts that the Fed will start cutting rates around the midpoint of 2024. “The takeaway here is we know the construction sector is an extremely interest-rate-sensitive portion of the economy, particularly in sectors like the residential market,” says Branch. “We think that by the end of the year, the U.S. economy is going to be on much more stable footing, which should create more opportunity in the construction market.”

Extras

- Dodge estimates that U.S. gross domestic product growth will slow in 2024.

- The Congressional Budget Office forecasts GDP to speed up, averaging 2.4 percent a year from 2024 to 2027, in response to projected declines in interest rates.

2 | Inflation is still volatile but slowly stabilizing

The Federal Reserve’s latest macroeconomic projections indicate a gradual reduction in inflation rates, averaging 2.5% in 2024, decreasing to 2.2% in 2025 and aligning with the Fed’s 2% target by 2026.

In terms of major economic indicators, inflation has remained at the top of the list over the past year. “We’ve seen significant progress over the last year,” says Kermit Baker, chief economist, American Institute of Architects. “A year ago, [the numbers] were a little over 8%. A few months ago, we saw them hit a low of 3%; they’ve come down dramatically. Generally, we’re moving in in the right direction, even though we’re not done with the inflation issue yet.”

Alex Carrick, chief economist, ConstructConnect, shares the sentiment on falling rates. “As interest rates stabilize and then begin to decline after Q1 or Q2 of next year, the homebuilding sector will revive.”

“What we’re seeing from an interest rate perspective, it’s hard for developers to make the returns, and they’re going to seek returns elsewhere,” says Jay Bowman, principal, FMI Corp., referencing private construction.

Extras

- Credit should start easing during the back half of 2024, but the banking sector will continue to be skittish, says Branch.

- Construction expenditures are forecast to increase 3.7% yearly in nominal terms through 2024, according to Construction: United States.

3 | Material price inflation about to turn

Talk in the construction industry has been dominated by the issue of bid and material prices, and Dodge’s Branch says that the industry will continue to see good news.

“It [composite index of building materials] is contracting after that steep run-up that we saw in the wake of the pandemic. And bid prices are starting to be essentially flat from where they were last year. We’re going to see continued relief in bid prices, contracting a little over the coming months through Q1 and maybe even early Q2 of next year, but that contraction is also going to be brief, and we’ll start to see them re-accelerate. They’ll return to more normal growth, somewhere in the 3% to 5% year-over-year range.”

Supply chains also improved in 2023, with the Global Supply Chain Pressure Index hitting a historical low in October 2023 and almost all material divisions seeing stable or improving lead times, showing that supply disruptions are in the back mirror, for now, according to real estate and investment management JLL Capital Markets. In 2024, slowing private-sector construction starts should keep supply chain pressure manageable, but the current pipeline and increase in publicly funded construction is anticipated to prevent price reductions.

4 | Labor challenges continue

“The number of people hired has been tailing off. You might think that indicates a declining demand for workers, but I think it indicates how hard it is to find workers to fill those positions. The unemployment rate in construction has come all the way down to the same level as the overall economy, to 4% or less, and that’s really exceptional.” Ken Simonson, chief economist, Associated General Contractors of America

Limited labor availability is expected to persist for the long term, according to the U.S. Bureau of Labor Statistics. Due to ongoing shortages and an increase in people leaving the industry, overall growth of the construction labor force will slow from its current, already inadequate, pace in 2024, severely limiting how many projects owners and developers can take on. While advancements in technologies can ease some of these pressure points caused by the labor market, it cannot fully replace the need for labor.

In North America, as the industry faces skilled labor shortages and falling productivity—competency and efficiency will be increasingly valuable among the workforce. Retention and upskilling are critical for the next year and beyond.

“The big challenge for contractors is going to continue to be finding workers,” says Simonson. “And I think that will be with us for many years.”

Companies may wish to take advantage of broader incentives, like the IRA tax credits available for companies who hire registered apprentices, which may build demand for apprenticeship programs, potentially expanding workforce training opportunities and benefitting employers.

Extras

- The U.S. Bureau of Labor Statistics projects that the labor force participation rate will continue to decline in 2024, although at a slower rate than that seen before the onset of the 2007–09 recession, falling 2.0 percentage points to 60.9% in 2024.

- The recent United Auto Workers strike took a bit out of Q3 and Q4 2023 GDP, says Branch, and might eat into economic output in Q1 2024, if there is labor action.

- Simonson forecasts that construction wages will rise 5% to 7% over the next year, the last increase of its kind since 1980.

- The Associated Builders and Contractors report the industry needs more than 342,000 new workers in 2024, and expect an increase in staffing in the first half of 2024.

5 | Geopolitical conflicts and trade tensions loom

Geopolitical risk is significant. Dodge forecasts that “tensions will start to ease in the coming three to six months.”

The Israel-Hamas conflict raises concerns about potential wider Middle East tensions, possibly impacting energy and other raw material prices. U.S. sanctions on Iran and possible retaliatory actions, including threats to the Strait of Hormuz, could further escalate these issues. And the ongoing tensions between the U.S. China could also stoke inflation.

In February, the Aluminum Extrusion Council reported on the White House proclamation adjusting imports of aluminum into the U.S. and significantly increasing costs for aluminum smelted or cast in Russia. Tariff rates on most metals and metal products will double from 35% to 70%. U.S. imports of unwrought aluminum and alloys from Russia amounted to 191,809 tons, or roughly 4.4% of the more than 4.4-million-ton total last year, compared with 8.9% in 2018 and 14.6% in 2017.

Rising energy prices and geopolitical tensions are new risks added to the matrix that Dodge examines. Branch also cited rising tensions in Russia, Ukraine and the Middle East as possible obstacles in the coming year. “Geopolitical risk remains intense,” he says, but Dodge forecasts that “tensions will start to ease in the coming three to six months.”

Extras

- The U.S. ban on exports of certain chips to China, including those by Nvidia and Intel, aims to limit their use in AI applications, adding to supply chain disruptions.

- The U.S. initiated a 200% tariff on all Russian-made aluminum in February 2023, which applies to about $2.8 billion worth of materials.

6 | Commercial construction edges lower

“The outlook for data centers seems almost unbounded.” Alex Carrick, Chief Economist, ConstructConnect

The commercial sector, which includes stores, offices, warehouses and hotels is expected to fall 6% to $156 billion in 2023, then another 2% to approximately $153 billion next year, Dodge predicts. “If you pull the warehouse sector out of that minus 2%, construction starts for commercial are actually positive,” says Branch.

Connor Lokar, senior forecaster, ITR Economics, who delivered the annual economic forecast keynote presentation at GlassBuild America concurs on non-residential construction lags. “For companies on the non-residential side, it has been great. … And next year should be great, or at least good. But be careful for what comes next,” Lokar says. “You’ll be in recession by end of 2024.”

On the public side of the commercial market, education and healthcare projects are moving slowly to start, which could be due to labor, costs or materials challenges. With private-side hotel and multi-family construction projects, market conditions may not be especially supportive right now. “What this says to me, is that projects are going into the queue, working their way through the planning cycle, to make sure that the market conditions in 2024 will be supportive,” says Branch. “If the signs indicate a good market, they want to be ready to move those projects forward. Once the economy is a little more stable, these projects will start moving through to groundbreaking.“

Warehouses—Starts in structural decline

The decline “really comes down to one sector, and it’s the warehouse sector,” says Branch. Amazon, which accounted for 16% of all warehouse construction, “essentially stepped aside,” which required a “realignment that continues in 2024” for warehouse construction, he adds. Dodge forecasts warehouse starts will end 2023 down 18%, followed by an additional 11% next year.

Branch attributes this due to warehouse construction, previously strong due to the rising popularity of online shopping, entering a cooling off period. “I hesitate to call this an economic downturn,” Branch said, but rather a “recalibration” necessary after “one player [steps] out.”

Hotels—Slowing economy hurting hotel starts

Hotel starts are down 5% in 2023 but will increase 16% in 2024. An extremely competitive sector, in the wake of the Great Recession, hotel starts really accelerated, but interest rates and tightening lending standards choked off development in 2023.

“Hotel fundamentals are very solid,” says Branch, particularly in the high-end market. “I hate to call anything recession proof, but those luxury and upscale projects are moving ahead whether the economy is slowing or not.”

Branch thinks that hotel chains are betting on a big return in business travel, that business travel will continue to grow, but will stay well below pre-pandemic levels. “The lower-middle hotels where most business travelers stay and extended-stay class of hotels, I think those are more about value,” adds Branch. “I think that comes into play more in 2024.

Offices—Office construction under stress

Office starts are expected to decline slightly, at a rate of 2%, in 2024, following two years of growth at a rate of 30% in 2022, and an additional 5% in 2023. While demand for traditional office space still suffers in the wake of the pandemic, data centers are expected to have “aggressive growth” in 2023 and 2024, says Branch. “When we pull out data centers, the 2% drop in overall office construction drops further by 6%.”

“If you look at office occupancy, it’s been sitting around 50 percent,” says Branch. “Office vacancy rates [are] sitting around 18%, up 140 basis points from where they were a year ago. Core office construction never gets back to where it was in 2019. We continue to believe here that remote and hybrid is going to continue to be a driving force in the employer employee relationship.”

Data center starts are still rising from 2022’s meteoric 140% jump. Dodge forecasts a 9% increase in 2024 following 2023’s 14% increase, but says to expect some deceleration in 2024 and a flattening out in 2025.

Alex Carrick, chief economist, ConstructConnect, also singles out data centers in ConstructConnect’s forecast as the bright spot in the office market. “The high-office-vacancy real estate sector may cause grief for lenders, as more leases will be expiring, and allowed to lapse, and rent collections will suffer,” he says, “[but] with more forays into artificial intelligence, virtual reality gaming, blockchain accounting and cybersecurity awareness, the outlook for data centers seems almost unbounded.”

Retail—Retail construction starts edge up in 2024

“Retail is probably the strongest link between the residential sector and the non-residential sector,” says Branch. “There’s a 12-month lag between the start of single family and the start of a retail development. But e-commerce kind of broke that. There’s still a lot of retail to residential development going on, relative to what we saw in the wake of the Great Recession.”

Dodge believes that the slow residential market is holding back retail starts, but that will change in 2024 with an increase of 9%, both from renovations and additions to existing buildings of top retail chains and the growing trend of residential construction moving from urban areas into the suburbs and even further out into the rural areas of the country.

“Rural construction for non-residential has actually picked up to about $10 billion in activity over the last couple of years,” says Branch. “It’s an area where the building stock has not kept up with the current population growth, and we’re seeing a lot of retail activity. We think that continues in 2024 with another gain here in retail starts, but project mix is very important.”

Extras

- FMI Corp. predicts that private commercial work is set to decline 8.9% in 2024.

7 | Institutional building to ease in 2024

Institutional construction starts are projected to increase 3% in 2024, following the upward trend of 7% in 2023 and 23% in 2022.

“There’s a lot more diversity here in project type, project size and geography too,” says Branch. “To me, this says a lot more about stability in the institutional market.”

Education—K-12 starts larger, but more volatile than university

The largest institutional construction sector, K-12, colleges and universities, and educational laboratories, libraries and museums are a mixed story, according to Dodge. “Mostly state and local funding drives [them] and those budgets are in really solid shape,” says Branch. “On the bad side, demographics are shrinking on the school age population and mixed-college construction. Overall, demographics are weaker for colleges and universities than they are for K-12.”

“Looking at the total market,” adds Branch, “if I were to rank the three by growth opportunity, I would put the K-12 market at the top. I think the strongest growth market in education is the laboratory market, but it’s a smaller portion of the total overall. The college sector is much like the hotel sector; it’s extremely competitive on who has the best facilities.”

Healthcare—Clinics, Hospital Construction to Fuel 2024

Among the stronger sectors is health care, which FMI forecasts will end 2023 up 9.4%, with an additional increase of 5.6% in 2024. While hospital construction has been relatively flat, medical office buildings have had a “meteoric rise” in the past 10 years, says Bowman. Once just representing one-fifth of the amount spent on construction of hospitals, he adds: “I believe [by] 2027 that we will have more spending on medical office buildings than we will on hospitals.”

Dodge predicts that clinic and hospital construction will fuel 2024, increasing 5%, and ranking clinics as the strongest and above trend, with hospitals right at trend, and the nursing home sector bringing down the average. Urgent-care centers, located mostly in suburban strip malls, are part of the retail growth happening in the suburbs, and signal a positive sign for healthcare clinic construction.

“We are starting to see reinvestment in the healthcare and hospital market. Clinics are looking more stable, much like hospitals, and both have been relatively flat over the past few years in terms of construction activity,” says Branch. “The nursing home side has fallen significantly, with construction about half of what it was pre-pandemic.”

Extras

- Dodge expects corporate campuses to pick up strength again in 2024.

- In 2022, square feet for K-12 was nearly five times the size of the post-secondary market.

“Commercial construction pretty much moves lock-step with the economy, and follows the single-family market,” says Branch. “The economy slows down construction, and commercial starts slow down with it.”

8 | High rates, lending standards hurting residential starts

“There’s a growing sense here that the single-family market is at least past the bottom.” Richard Branch, Chief Economist, Dodge Construction Network

There’s a strong correlation between residential construction and the non-residential building sector; single-family construction organically leads the construction sector into decline or recovery, according to Branch. “Residential leads commercial buildings, like retail leads institutional buildings like hospitals and schools.”

The total dollar value of residential starts is expected to end the year down 13%, before rising 11% in 2024.

“The residential market split, with single family going one way towards a pseudo recovery, and multi-family going the other, peaking in December 2022, and falling since.” household formation is slowing, , people were cohabitating longer coming out of Covid, younger folks are moving back in with their parents, Credit is hard to get for multi-family construction… that’s going to push up vacancy rates. higher vacancy rates will suppress construction.

Alex Carrick shares the sentiment that falling rates are the key to a thriving residential market. “As interest rates stabilize and then begin to decline after Q1 or Q2 of next year, the homebuilding sector will revive.” ConstructConnect’s forecast predicts a 4.4% increase in 2024 for total residential starts, with a more robust 15% increase expected the following year.

Single-family—Starts tied to mortgage rate pressures

In the residential sector, Dodge predicts single-family construction will end this year down 12%, measured in units, before climbing 3% in 2024. Branch notes that while the bottom for single-family starts has passed, mortgage rates need to ease before the sector will see stronger growth.

“New home sales, tightly correlated to new home construction starts, are up 5% on a year-to-date basis,” says Branch. “With mortgage rates where they are, we’re not going to see a big run up in single-family construction anytime soon. People are still buying homes right now even with mortgage rates where they are.”

Branch believes that downward pressure on mortgage rates will come in Q1 2024, creating more stability and propagating single-family construction through late 2024 and 2025.

“The market needs lower interest rates for people to consider selling their homes that they refinanced when rates were low,” Lokar says.

Multi-family—Recalibration and increase for 2024

Multi-family work is expected to follow a similar pattern, dropping 13% by the end of 2023, with a 3% increase in 2024. Following a peak at the end of 2022, starts in this sector have declined, due in part to tightening credit standards for multifamily and commercial properties, as well as younger people cohabitating or living with family, lowering demand. Still, says Branch, this is simply a fall from the peak of activity. “[Before 2021], these are the highest levels for multi-family construction, going back to the ‘80s,” says Branch. “There’s still a lot of activity going on, so perhaps this is just a recalibration or a realignment following a little rush of development in 2021–2022.”

Companies that leaned into multi-family contracts during the sector’s boom of the last several years should prepare for slowdown in the near term, Lokar says. “If you’ve been living off multifamily, [the sector] is entering recession,” he says. “Starts were down 28.1% in the last quarter, and permit pulls have cratered.”

“The point I want to make in multifamily is that even though the national market and some of the indicators are suggesting weakness, there are pockets of opportunity and growth in the multifamily space,” adds Branch. “I think that recovery [going into] 2024 is going to develop later for the multifamily market. Single-family goes first, multifamily comes after.”

Extras

- The National Association of Home Builders projects that residential construction will drop 3.4% in 2024, single-family will rise 3.7% in 2024, and multifamily will see a 17.3% decrease next year.

- Lokar believes that the single-family market is now bounding into recovery, but that multi-family is heading for a tough year.

- FMI Corp. predicts the residential market will fall 7.1% in 2024; private multi-family could be down close to 20% by 2025.

- Branch says consistent new home sales around the 700,000-unit range through the first nine months of this year are needed; currently it’s at about 684,000 units a month.

9 | Manufacturing to lead the way

After a 217% increase in 2022, manufacturing will fall slightly at a rate of 5% by the end of 2023, before rising 16% in 2024, Dodge predicts.

While the increase is “not a surprise, considering the impact of the CHIP and Inflation Reduction Acts,” says Branch, he also notes that the availability of labor has been an obstacle in 2023, causing the slight downturn and pushing several projects into the coming year.

In line with the Dodge forecast, the FMI outlook highlights manufacturing as a robust market going into 2024. “The value of manufacturing put-in-place construction is set to increase 58.2% in 2023, with an additional 15.1% in 2024, according to Bowman.

Extras

- A record $102 billion dollars in public funds boosted manufacturing construction activity in 2022; with a 5% drop in 2023 and forecasted to go up 16% in 2024.

10 | Eye on the horizon, sectors to watch

Large airport expansions in Colorado, Texas, Montana, Missouri, Iowa and Minnesota are boosted by cash infusions from the Infrastructure Investment and Jobs Act.

Energy advocates are keeping an eye on the 2024 U.S. election to inform how it may shape, or re-shape, energy transition policy. In its 2024 Engineering & Construction Industry Outlook, Deloitte believes that sustainable practices and technology advancements are likely to shape the industry in 2024, as key pieces of the Infrastructure Investment and Jobs Act, the Inflation Reduction Act, and the CHIPS Act flow into the industry. The U.S. is also prioritizing sustainable construction through its Federal Buy Clean Initiative, which specifies more than $2 billion for the procurement of lower-carbon construction materials for use in federally funded projects.

For infrastructure, Dodge predicts that 2024-2025 might be the best years for growth, thanks to delayed appropriation bills finally being passed. “By the midpoint of next year, we should start to see acceleration in the forecast,” says Branch. Under this sector, sewage and waste-disposal systems, and water-supply systems are forecasted to rise 13% and 21%, respectively, in 2024, which are necessitated by the demands of a growing population. “There is some linkage here between new single-family and multi-family development,” adds Branch, “so it should get a bit of an extra kick here as we go into 2024.”

Finally, aviation projects are taking off. Large airport expansions in Colorado, Texas, Montana, Missouri, Iowa and Minnesota are boosted by cash infusions from the Infrastructure Investment and Jobs Act, which designates $15 billion over five years for terminals, safety and sustainability efforts, and airport-transit connections. Of that, $2.89 billion became available for airport projects in fiscal year 2023.

Tara Lukasik is Managing Editor of Glass Magazine and Window + Door Magazine. Email her at tlukasik@glass.org. This article originally appeared in the January/February 2024 issue of Glass Magazine, a publication of the National Glass Association, and is reprinted with permission.